AML Compliance

Last Updated: March 2026

Based On Regulatory Guidance And Industry Data

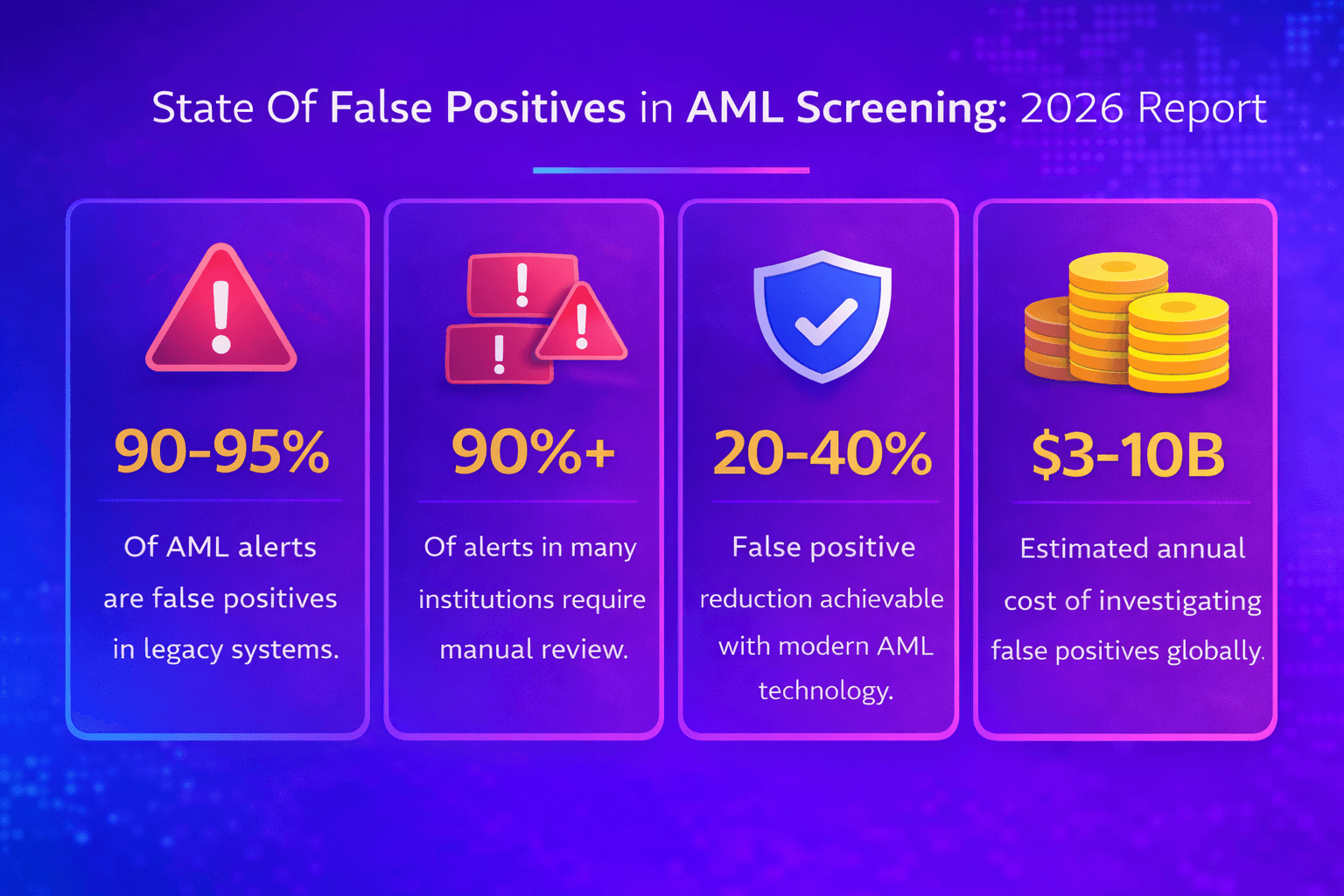

AML false positive rates typically range between 85% and 95%, meaning most compliance alerts do not represent genuine financial crime risk. This imbalance creates significant operational inefficiencies across financial institutions.

False positives remain one of the most persistent and costly challenges in Anti Money Laundering screening. Financial institutions process vast volumes of alerts each day, yet only a small proportion result in confirmed suspicious activity.

Guidance from the Financial Action Task Force recommendations emphasises that risk based systems should balance detection accuracy with operational efficiency. However, many institutions continue to experience excessive alert volumes due to limitations in legacy systems and data quality.

From a practical compliance perspective, false positives are not just a technical issue. They directly affect alert investigation workflows, staffing requirements, and the ability to detect genuine financial crime efficiently.

Modern customer screening systems and payment screening infrastructure are increasingly designed to reduce unnecessary alerts through better contextual matching and data enrichment.

This report combines regulatory insights, industry benchmarks, and operational analysis to provide a clear and evidence based view of false positives in 2026.

The False Positive Efficiency Gap

Based on industry benchmarks, compliance teams spend up to 90% of their time investigating alerts that do not result in action. This creates what can be described as the False Positive Efficiency Gap, the gap between alert volume and actual risk detection.

This gap is not simply an operational inconvenience. It represents a structural inefficiency embedded within many compliance systems.

False positives are not just noise. They are a systemic issue that also contributes to broader concepts such as alert fatigue, explored in more detail within false positives and related compliance terminology. that directly impacts detection quality, operational scalability, and regulatory confidence.

The False Positive Burden In AML

In 2026, financial institutions are not limited by their ability to detect potential risk. They are limited by their ability to process it efficiently.

This creates what can be described as the False Positive Burden — where the majority of compliance effort is consumed by alerts that do not result in actionable outcomes.

Key False Positive Statistics In AML Screening

Understanding false positives requires a grounded view of industry data. While exact figures vary by institution, multiple regulatory bodies and studies consistently highlight extremely high false positive rates across screening systems.

Industry Benchmarks

Metric | Verified Range | Source Context |

|---|---|---|

Average False Positive Rate | 85% – 95% | Widely cited across industry studies and regulatory discussions |

Alerts Resulting In SARs | 1% – 5% | Regulatory reporting benchmarks |

Average Investigation Time Per Alert | 20 – 60 minutes | Industry operational estimates |

Daily Alerts (Large Institutions) | 10,000+ | Large bank transaction monitoring volumes |

Regulatory commentary from the Financial Conduct Authority financial crime guidance has repeatedly highlighted inefficiencies in transaction monitoring frameworks and the disproportionate volume of alerts that do not lead to suspicious activity reports.

For broader context, see AML compliance statistics and sanctions screening statistics.

What This Data Actually Means

The statistics above are not just abstract figures. They reflect consistent operational patterns observed across financial institutions globally. Interpreting this data helps explain why false positives remain such a persistent issue.

The data highlights several consistent patterns across institutions:

A significant majority of alerts generated by AML systems do not correspond to actual financial crime risk

Compliance teams allocate substantial time to reviewing alerts that do not lead to suspicious activity reports

High false positive rates are driven more by system design and data limitations than by investigator performance

What False Positives Actually Cost Per Day

To understand the real impact of false positives, it is necessary to translate percentages into operational workload.

A financial institution processing 10,000 alerts per day with a 90% false positive rate and an average investigation time of 30 minutes per alert would generate:

9,000 false positive alerts per day

4,500 analyst hours spent on non actionable investigations

Equivalent workload of over 500 full time analysts annually

This level of inefficiency significantly increases the cost of compliance operations and reduces the capacity to focus on genuine risk.

This is why solutions focused on false positive reduction in sanctions screening, improved alert triage processes, and structured decision frameworks such as compliance decision logging are becoming critical for scaling compliance functions.

The 4 Drivers Of False Positives In AML Systems

False positives are not random. They are driven by four core structural factors that exist across most screening environments.

1. Data Quality Limitations

Incomplete or inconsistent customer data creates ambiguity during screening. Missing identifiers such as date of birth or nationality make it difficult to distinguish between individuals with similar names.

Improving watchlist data management and customer data quality is one of the most effective ways to reduce unnecessary alerts, a challenge also identified by the Bank for International Settlements data quality analysis.

2. Matching Logic Constraints

Name matching systems often rely on fuzzy logic, which increases match sensitivity but can generate incorrect matches when not properly tuned.

Optimising techniques such as fuzzy matching thresholds helps balance detection accuracy and alert volume.

3. Watchlist Design And Scope

Overly broad or poorly structured watchlists increase the likelihood of irrelevant matches. Effective list segmentation and normalisation are essential.

4. Rule Configuration And Static Thresholds

Legacy systems rely heavily on static rules that trigger alerts without sufficient contextual understanding. These systems cannot adapt to behavioural patterns or evolving risk profiles.

The Cost Of False Positives In Compliance Operations

False positives create a measurable financial and operational burden for financial institutions. These costs extend beyond technology into staffing, workflows, and customer experience.

Operational Cost Breakdown

Cost Area | Impact |

|---|---|

Analyst Time | High manual workload per alert |

Compliance Staffing | Increased hiring requirements |

Technology Usage | Inefficient utilisation of systems |

Customer Operations | Delays in onboarding and transactions |

Analysis from the International Monetary Fund highlights the rising global cost of compliance, with financial institutions spending billions annually to meet regulatory expectations.

Financial Impact Insights

The financial implications of false positives extend beyond headline costs. They influence how institutions allocate resources, structure teams, and manage operational efficiency.

From an operational standpoint, the financial impact of false positives can be summarised as follows:

Significant investment in compliance teams to manage alert volumes

Reduced productivity due to time spent on low risk investigations

Increased cost per customer onboarding and transaction processing

How False Positives Impact Financial Institutions

False positives do not only affect compliance metrics. They have a direct impact on how financial institutions operate, scale, and manage risk. From operational efficiency to customer experience and regulatory expectations, excessive alert volumes influence multiple layers of the organisation.

Reduced Operational Efficiency

High volumes of alerts create bottlenecks in investigation workflows, limiting the ability of teams to scale effectively.

Analyst Fatigue

Continuous exposure to low value alerts increases cognitive load and raises the risk of missing genuine suspicious activity.

Customer Experience Issues

Screening delays can slow onboarding processes and interrupt legitimate transactions, negatively impacting customer experience and trust.

Increased Regulatory Pressure

Regulators increasingly expect institutions to demonstrate that their systems are both effective and proportionate, particularly in relation to alert quality and decisioning.

False Positives Vs True Positives

To properly evaluate AML screening performance, it is important to understand the relationship between false positives and true positives. These two outcomes determine whether a system is generating meaningful alerts or simply creating operational noise.

Alert Outcome Comparison

The following breakdown illustrates the typical distribution of alert outcomes across financial institutions. While exact figures vary, the imbalance between false and true positives remains consistent across most screening environments.

Alert Type | Percentage |

|---|---|

False Positives | 85% – 95% |

True Positives | 1% – 5% |

Insight

The problem is no longer detection. It is precision. Most compliance effort is directed towards alerts that do not result in meaningful action.

How False Positive Rates Are Changing In 2026

Several key trends are shaping how institutions approach false positive reduction.

Adoption Of AI And Machine Learning

Machine learning models improve screening accuracy by analysing behavioural patterns and contextual relationships, reducing reliance on static rules.

Real Time Screening Requirements

With the growth of instant payments, institutions must process transactions in real time. This requires more accurate screening systems that minimise unnecessary alerts.

Solutions built on real time screening infrastructure are designed to handle this shift.

Improved Data Management

Enhancing data quality through validation, enrichment, and standardisation reduces ambiguity and improves matching precision.

Shift Towards Risk Based Models

Institutions are increasingly adopting risk based approaches that adjust screening sensitivity based on customer profiles and transaction context.

Key Takeaways

The findings in this report highlight several consistent conclusions about the current state of AML screening and compliance operations.

False positives remain a dominant feature of compliance workflows

Up to 90% of compliance effort may be spent on non actionable alerts

Data quality and system design are primary drivers of inefficiency

Modern compliance strategies focus on precision rather than volume

Institutions that reduce false positives do not simply improve efficiency. They improve detection quality and regulatory defensibility.

How Financial Institutions Can Reduce False Positives

Reducing false positives requires a combination of data improvements, system optimisation, and strategic changes to screening approaches. The following areas represent the most effective starting points.

Improve Data Quality

Accurate and complete customer data reduces ambiguity and improves screening precision.

Use Intelligent Matching Techniques

Advanced matching approaches improve detection accuracy while reducing unnecessary alerts.

Optimise Watchlist Management

Maintaining high quality, relevant watchlists ensures fewer irrelevant matches.

Implement Risk Based Screening

Applying risk based thresholds allows institutions to focus resources on higher risk cases while reducing noise.