AML Compliance

Anti money laundering compliance has become one of the most complex and resource intensive obligations faced by financial institutions. Governments continue to strengthen financial crime regulations while criminals adopt increasingly sophisticated methods to move illicit funds through the global financial system.

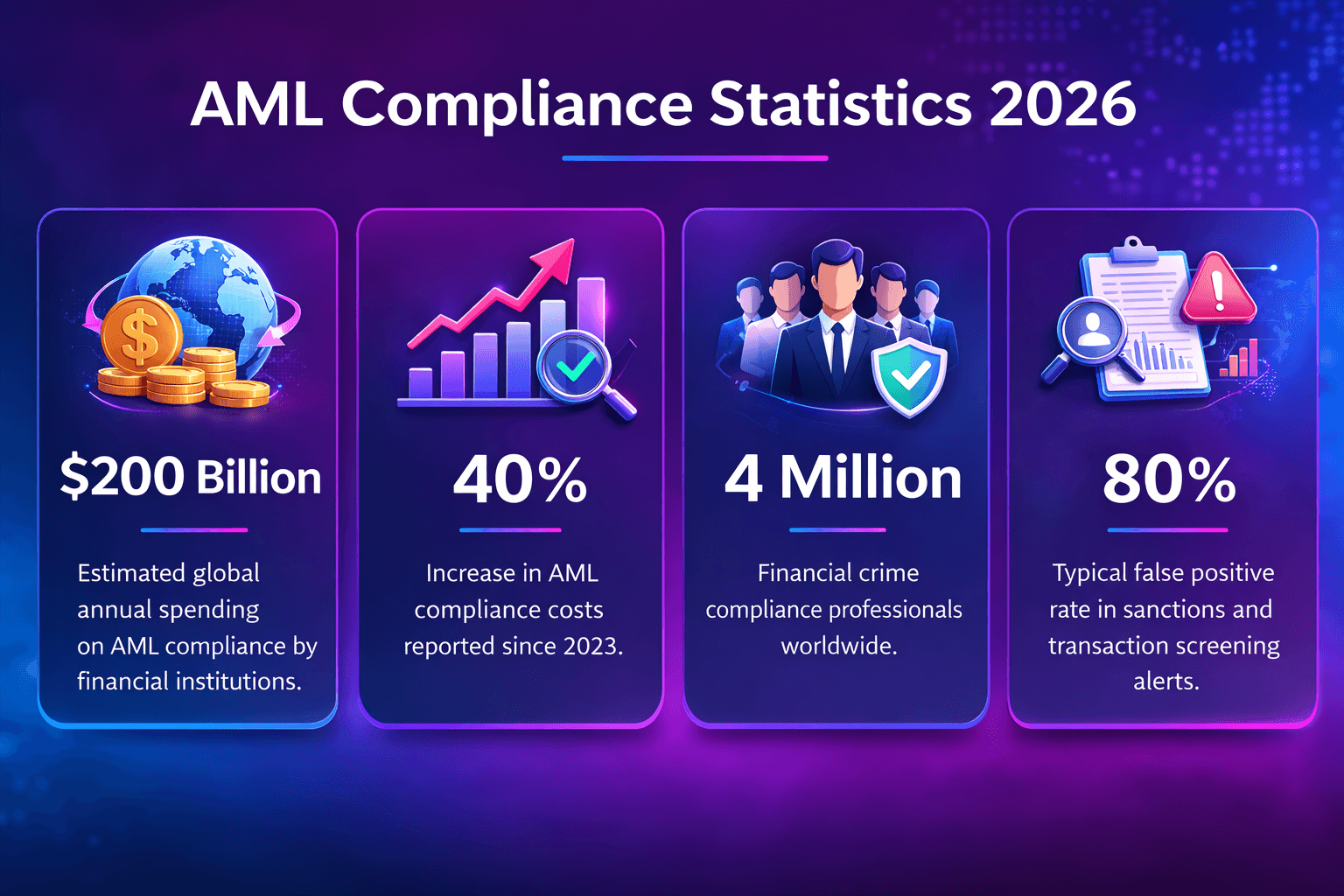

Understanding the scale of financial crime and the effectiveness of compliance controls requires analysing reliable data. AML compliance statistics provide insight into the volume of suspicious activity reports submitted each year, the scale of global money laundering, and the regulatory penalties imposed on institutions that fail to maintain adequate controls.

For compliance leaders, these statistics help contextualise operational risk and highlight where improvements in screening, monitoring, and investigation processes may be required.

This guide summarises the most important AML compliance statistics for 2026 and explains what they reveal about the evolving financial crime landscape.

The Estimated Scale Of Global Money Laundering

One of the most widely cited statistics in financial crime research is the estimated scale of global money laundering. According to analysis discussed by the United Nations Office on Drugs and Crime global money laundering estimate, between two and five percent of global GDP may be linked to illicit financial flows each year.

This estimate represents trillions of dollars moving through financial systems annually. The scale of this activity illustrates why governments continue to expand AML regulation and strengthen enforcement actions against financial institutions that fail to detect suspicious transactions.

Although exact figures are difficult to measure due to the hidden nature of financial crime, the data demonstrates that money laundering remains a significant global economic threat.

Suspicious Activity Reporting Volumes

Financial institutions around the world submit millions of suspicious activity reports each year. These reports are filed with national financial intelligence units whenever unusual financial behaviour suggests potential money laundering or terrorist financing.

For example, the Financial Crimes Enforcement Network reporting statistics indicate that millions of suspicious activity reports are filed annually in the United States alone.

These reports allow financial intelligence authorities to identify patterns across institutions and detect complex financial crime networks that would otherwise remain hidden.

However, high reporting volumes also illustrate the operational burden placed on compliance teams responsible for investigating alerts before determining whether a report should be filed.

Global AML Regulatory Fines

Regulatory enforcement actions continue to increase as authorities scrutinise financial institutions' compliance programmes. Banks and financial services providers that fail to maintain adequate AML controls may face substantial penalties.

Analysis of enforcement trends published by the Bank for International Settlements financial crime compliance research highlights the growing importance regulators place on financial crime risk management.

Over the past decade, global AML related fines have reached billions of dollars. These enforcement actions typically arise from failures in areas such as sanctions screening, transaction monitoring, and suspicious activity reporting.

For compliance teams, these penalties demonstrate the importance of maintaining reliable detection systems and documented investigation procedures.

Screening Alert Volumes Inside Financial Institutions

Internal compliance statistics often reveal that the majority of screening alerts generated by AML systems are false positives. Name similarities, incomplete data, and transliteration variations frequently trigger alerts that investigators must review manually.

This operational reality means that compliance teams must evaluate very large volumes of alerts in order to identify a small number of genuine financial crime risks.

Effective screening systems help reduce unnecessary alerts by improving matching accuracy. Tools such as structured customer screening systems allow institutions to compare names and identifying attributes against sanctions lists more precisely.

Reducing false positives allows investigators to focus more effectively on genuinely suspicious activity.

Transaction Monitoring Data Volumes

Transaction monitoring systems analyse extremely large datasets in order to detect unusual behaviour patterns. Large banks may monitor millions of transactions every day, particularly when operating across multiple payment networks.

These monitoring systems identify patterns such as unusual transaction volumes, rapid movement of funds, or transfers involving high risk jurisdictions.

When potential risks are identified, alerts are generated and reviewed through structured alert adjudication workflows that help investigators determine whether activity should be escalated or reported.

The volume of transactions analysed by these systems highlights the importance of automation and efficient investigation processes within AML programmes.

Regulatory Expectations Continue To Increase

AML compliance statistics show that regulators expect financial institutions to maintain increasingly sophisticated financial crime controls. Authorities now expect banks to demonstrate not only that systems exist, but also that those systems operate effectively in practice.

This includes maintaining reliable sanctions data, monitoring transactions continuously, and documenting investigation decisions.

Many organisations therefore invest in technologies such as advanced screening infrastructure supported by a watchlist management platform capable of consolidating sanctions lists from multiple authorities.

These systems help institutions maintain accurate sanctions data and respond quickly when regulatory lists change.

Operational Challenges Revealed By AML Data

Statistical analysis of AML programmes highlights several common operational challenges.

High Investigation Workloads

Large volumes of alerts require investigators to review significant amounts of information before determining whether suspicious activity should be reported.

Data Quality Limitations

Incomplete or inconsistent customer data can make screening and monitoring less effective.

Regulatory Complexity

Institutions operating internationally must comply with multiple regulatory frameworks simultaneously.

Technology Integration

Legacy systems can make it difficult to integrate modern financial crime detection tools.

Addressing these challenges requires both strong governance and reliable compliance technology.

What The Statistics Mean For Compliance Teams

AML compliance statistics highlight the scale and complexity of financial crime risk management. While financial institutions have made significant investments in compliance infrastructure, the data suggests that operational improvements are still required in many organisations.

Institutions that combine reliable screening systems, efficient investigation processes, and strong governance structures are better positioned to manage the large volumes of data generated by modern financial systems.

Professional Insight And Operational Confidence

Understanding AML compliance statistics provides valuable context for compliance professionals responsible for managing financial crime risk. Data relating to suspicious activity reporting, enforcement actions, and global money laundering estimates helps organisations benchmark their compliance programmes against industry expectations.

Practical Experience

Compliance professionals frequently observe that improving data quality and investigation workflows significantly reduces operational pressure within AML programmes.

Technical And Regulatory Expertise

Strong AML programmes require both regulatory knowledge and technical infrastructure capable of analysing large volumes of financial data.

Building Confidence In Controls

When institutions can demonstrate that their screening and monitoring systems operate effectively, they are better positioned to satisfy regulatory expectations.

People First Compliance Content

Financial crime compliance ultimately depends on investigators who analyse alerts and interpret potential risk indicators. While technology enables institutions to analyse large volumes of data, human judgement remains essential when determining whether financial activity is suspicious.

Educational resources such as this guide help compliance professionals understand how financial crime statistics reflect the operational realities of AML programmes.

Next Steps For Your Organisation

As AML regulations continue to evolve, organisations must ensure that their compliance frameworks remain aligned with regulatory expectations and operational realities.

If your organisation is reviewing its financial crime controls or evaluating improvements to its screening and investigation systems, explore how your compliance architecture compares with current industry practices.