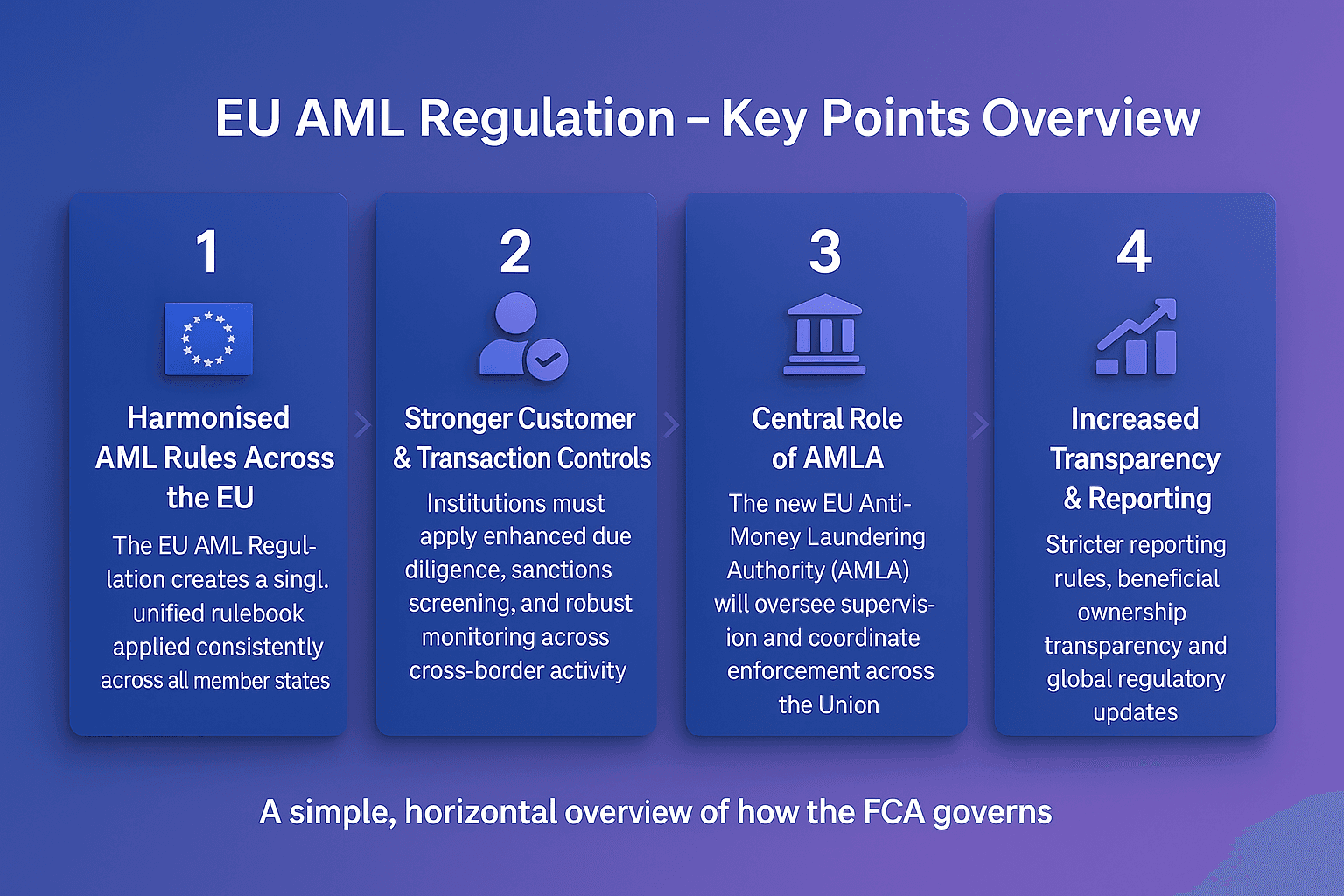

The EU Anti-Money Laundering Regulation (Regulation (EU) 2024/1624), informally referred to as the EU AML Regulation 2025, marks the most significant reform of Europe’s financial crime framework in two decades. It replaces the patchwork of national AML laws derived from previous directives with a single, directly applicable rulebook that binds all Member States equally.

This Regulation ensures that core compliance obligations, such as customer due diligence, transaction monitoring, and reporting standards, are interpreted and enforced uniformly across the EU. It forms part of the European Commission’s broader AML Package, adopted in June 2024, which also includes the creation of the European Anti-Money Laundering Authority (AMLA) and a companion directive to address country-specific procedural issues.

Together, these measures are designed to close regulatory gaps, eliminate inconsistencies, and deliver a unified, high-integrity framework for preventing money laundering and terrorist financing within the European Union.

Definition & Legal Basis

The EU AML Regulation establishes harmonised obligations for financial institutions and designated non-financial businesses across all 27 Member States. Unlike previous AML Directives (such as AMLD4 and AMLD5), it does not rely on national transposition, meaning its provisions apply directly and uniformly to all entities in scope once in force.

Published in the Official Journal of the European Union in June 2024, the Regulation will begin applying in July 2027, creating a standardised AML/CTF framework that leaves no room for interpretive divergence between countries.

Its introduction responds to long-standing concerns that varying national implementations of earlier AML Directives allowed financial crime risks to shift between jurisdictions, a weakness exploited by cross-border criminal networks.

Purpose And Objectives

The central purpose of the EU AML Regulation is to unify AML compliance obligations across the EU, ensuring a level playing field for financial institutions and a consistent enforcement framework for regulators.

Its key objectives include:

Removing discrepancies between national AML laws and creating a single, directly enforceable rulebook.

Enhancing the effectiveness of AML supervision through the European Anti-Money Laundering Authority (AMLA).

Strengthening due diligence, monitoring, and reporting standards for both traditional and digital financial services.

Expanding the scope of obliged entities to reflect evolving risks, including those linked to crypto-assets and high-value goods.

Facilitating cooperation, data exchange, and joint supervision among national authorities.

In essence, the Regulation seeks to transform AML compliance from a fragmented national system into a single, coherent European framework, much like how the Single Supervisory Mechanism unified banking oversight.

Key Features And Innovations

The EU AML Regulation introduces a number of structural and operational reforms aimed at improving consistency, transparency, and enforcement across the Union.

At its core, the Regulation replaces the varying national implementations of previous directives with a single EU-wide AML rulebook. Financial institutions, payment providers, and non-financial obliged entities will now follow the same definitions, thresholds, and control requirements, regardless of where they operate in the EU.

It also broadens the range of obliged entities to include:

Crypto-asset service providers, such as exchanges and wallet operators.

Crowdfunding and investment platforms, recognising their role in cross-border financial flows.

High-value goods traders (including luxury car dealers and art market participants).

Professional football clubs and agents, reflecting emerging money-laundering typologies in sports finance.

Beyond scope expansion, the Regulation introduces uniform rules on customer due diligence, risk assessment, and record-keeping, as well as more prescriptive standards for PEP identification, high-risk third-country transactions, and cross-border cooperation between Financial Intelligence Units (FIUs).

By setting a common baseline for every Member State, the Regulation effectively ends “AML arbitrage”, the practice of exploiting weaker national regimes to obscure illicit flows.

Why The Regulation Matters

For compliance professionals and regulated institutions, the EU AML Regulation represents a paradigm shift. Instead of tailoring frameworks to multiple national laws, firms operating in Europe will now be able to align their programs to a single set of EU-level requirements.

This simplifies governance, reduces legal uncertainty, and enhances the quality of cross-border compliance, especially for global banks and fintechs managing complex, multi-jurisdictional structures.

For regulators, it provides a clearer mechanism to enforce consistent standards. By removing discretion in how AML rules are transposed, supervisors can focus more on risk outcomes rather than procedural differences.

The creation of AMLA further amplifies this shift. AMLA will have both direct supervisory authority over certain high-risk cross-border institutions and a coordinating role to ensure national regulators apply the Regulation in a uniform manner.

Implementation Timeline

The EU AML Regulation entered into force in 2024 and will apply from 10 July 2027. Specific provisions for certain sectors, such as professional football and virtual asset services, will take effect later, by July 2029.

In parallel, AMLA is scheduled to become operational by mid-2025, based in Frankfurt. Its initial focus will be building supervisory teams, developing reporting frameworks, and identifying cross-border entities to be placed under direct oversight.

Financial institutions should therefore begin gap assessments now, evaluating how existing national compliance processes align with the new EU-wide standards. Systems for customer screening, payment monitoring, and transaction reporting must be flexible enough to integrate harmonised definitions and data requirements once the Regulation applies.

The Future Of EU AML Compliance

The EU AML Regulation is not simply a legislative update. It is a complete structural overhaul. By centralising supervision and codifying consistent standards, it aims to deliver a future where AML compliance is predictable, data-driven, and technologically enabled.

Looking ahead, the Regulation will likely encourage greater use of RegTech solutions, real-time data monitoring, and AI-assisted compliance tools to meet its stringent requirements. It also lays the groundwork for improved data sharing between Member States, paving the way for stronger cross-border investigations.

In combination with AMLA’s supervisory model, this Regulation will set a new global benchmark for coordinated financial crime prevention, one that other jurisdictions may emulate in the coming decade.

Strengthen Your AML Compliance Framework For The EU Rulebook

Preparing for the EU AML Regulation requires financial institutions to think beyond national compliance silos. Building systems capable of real-time risk detection, cross-border data alignment, and consistent monitoring standards will be key to readiness.

Modern solutions such as Customer Screening, Payment Screening, and Transaction Monitoring provide the foundation for regulatory alignment and efficiency under the upcoming rulebook.

Contact Us Today To Strengthen Your AML Compliance Framework

Frequently Asked Questions

It is a directly applicable EU law that creates a single, harmonised AML/CTF framework across all Member States, replacing many of the rules previously set out in national legislation.

What Is The EU AML Regulation?

When Will The Regulation Apply?

How Does It Differ From Previous AML Directives?

What Is AMLA’s Role Under The Regulation?

Which Entities Fall Under The Regulation?