AML Compliance

Real time payment systems are rapidly transforming global financial infrastructure. Networks such as Faster Payments, SEPA Instant, and other instant settlement platforms allow funds to move between accounts within seconds. While these systems provide significant benefits for consumers and businesses, they also introduce new challenges for financial crime compliance.

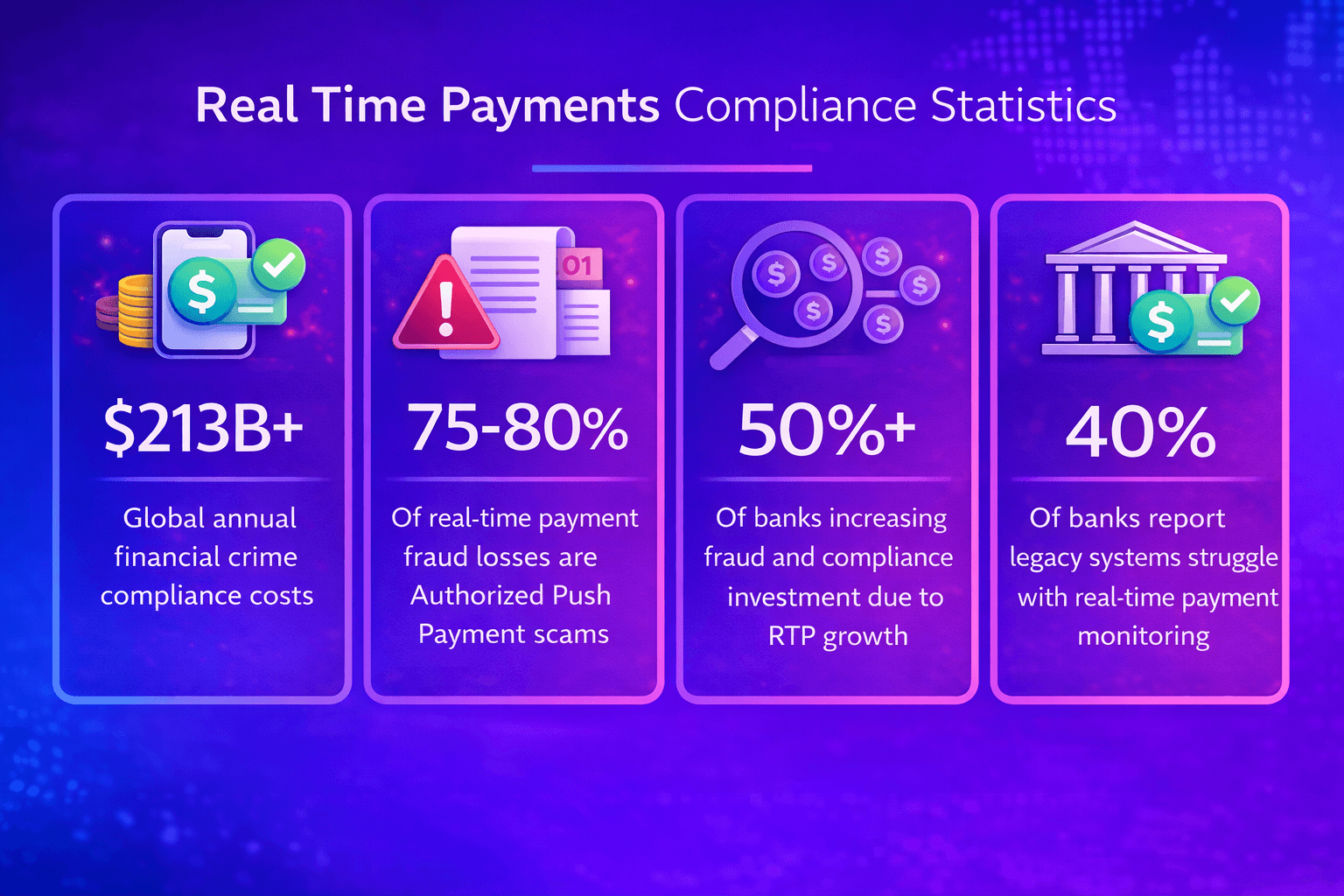

Compliance teams must ensure that sanctions screening, transaction monitoring, and fraud detection controls operate effectively even when payments settle almost instantly. Real time payments therefore require financial institutions to evaluate extremely large volumes of transactions with minimal processing delay.

Understanding real time payments compliance statistics helps organisations assess the scale of this challenge and identify the operational changes required to maintain strong financial crime controls.

Growth Of Real Time Payment Networks

Real time payment infrastructure has expanded rapidly over the past decade. Many countries now operate instant payment networks that allow individuals and businesses to transfer funds immediately rather than waiting for traditional settlement cycles.

Research discussed by the Bank for International Settlements on fast payments highlights how instant payment systems are becoming a core component of modern financial infrastructure. These systems process extremely high transaction volumes and require robust risk management frameworks.

As adoption continues to increase, financial institutions must ensure that their compliance systems can operate effectively within these high speed environments.

Transaction Volumes In Instant Payment Systems

Real time payment networks process very large transaction volumes. National payment systems can handle millions of transactions per day as consumers and businesses increasingly rely on instant transfers.

Each transaction must be evaluated for potential financial crime risk before funds are released. This means that screening systems must operate with extremely low latency.

Many institutions therefore integrate screening controls directly within payment processing infrastructure using modern payment screening systems that evaluate transactions in real time.

The ability to screen payments within milliseconds is essential for maintaining compliance while preserving the speed benefits of instant payment networks.

Fraud And Financial Crime Risks In Real Time Payments

The speed of instant payment systems can increase financial crime risks if compliance controls are not properly implemented. Once a real time payment is completed, the funds may be difficult to recover.

This means that institutions must detect potential sanctions exposure or suspicious activity before the payment is executed. Transaction monitoring tools therefore play a critical role in identifying unusual behaviour patterns.

Platforms supporting transaction monitoring controls allow institutions to analyse transaction patterns and identify potential financial crime risks in real time environments.

These systems help compliance teams detect suspicious behaviour even when payments occur within seconds.

Screening Alert Volumes In Instant Payment Systems

Because every payment must be screened before processing, instant payment networks generate large numbers of alerts that investigators must review. Even small percentages of potential matches can produce significant investigation workloads.

Compliance teams therefore rely on structured alert adjudication workflows to review alerts efficiently and document investigation decisions.

Efficient investigation processes are essential because payment delays can affect customer experience and operational performance.

Regulatory Expectations For Instant Payment Compliance

Regulators increasingly expect financial institutions to demonstrate that financial crime controls remain effective even within instant payment systems. Authorities emphasise the importance of maintaining sanctions screening, monitoring controls, and reporting procedures that operate effectively in high speed environments.

Guidance discussed by organisations such as the Financial Action Task Force digital payments risk guidance highlights how financial institutions must apply risk based compliance controls across emerging payment technologies.

These expectations require organisations to adapt their compliance architecture as payment infrastructure evolves.

Operational Challenges Revealed By Real Time Payment Data

Statistical analysis of instant payment systems reveals several operational challenges for compliance teams.

High Transaction Velocity

Payments occur within seconds, leaving little time for investigation.

Alert Investigation Pressure

Investigators must review alerts quickly to avoid delaying legitimate payments.

Data Quality Limitations

Payment messages may contain limited identifying information, making screening more complex.

Technology Performance Requirements

Screening systems must operate with extremely low latency while maintaining detection capability.

Addressing these challenges requires both advanced technology and well designed operational processes.

What Effective Real Time Payment Compliance Looks Like

Financial institutions that manage instant payment compliance successfully typically demonstrate several key characteristics.

Integrated Screening Infrastructure

Screening controls operate directly within payment processing pipelines.

Efficient Investigation Workflows

Compliance teams follow structured procedures when reviewing alerts.

Continuous Monitoring

Payment data is monitored continuously to identify suspicious behaviour patterns.

Strong Governance

Responsibilities for instant payment compliance are clearly defined across the organisation.

These practices help institutions maintain reliable compliance frameworks within high speed payment environments.

Professional Insight And Operational Confidence

Real time payments represent a major shift in financial infrastructure. While instant payment networks create new opportunities for innovation, they also increase the complexity of financial crime risk management.

Organisations that invest in reliable screening technology, efficient investigation workflows, and strong governance frameworks are better positioned to manage these challenges while maintaining regulatory confidence.

Practical Experience

Compliance professionals often observe that integrating screening systems directly within payment infrastructure significantly improves operational efficiency.

Technical And Regulatory Expertise

Managing instant payment compliance requires both regulatory knowledge and technical expertise in payment processing systems.

Building Confidence In Controls

When institutions demonstrate that their controls operate effectively in real time environments, regulators gain greater confidence in their financial crime frameworks.

People First Compliance Content

Financial crime compliance ultimately depends on investigators who analyse alerts and interpret potential risk indicators. Technology enables institutions to screen large volumes of transactions, but human expertise remains essential when determining whether activity represents a genuine financial crime risk.

Educational resources such as this guide help compliance professionals understand the operational realities reflected in real time payment compliance statistics.

Next Steps For Your Organisation

As instant payment systems continue to expand, financial institutions must ensure that their compliance controls evolve alongside payment infrastructure.

If your organisation is reviewing its real time payment screening or monitoring controls, explore how your compliance architecture compares with current industry practices.