AML Compliance

Instant payment systems are transforming the way money moves across the global financial system. Platforms such as Faster Payments, SEPA Instant, and other real time payment networks allow funds to be transferred and settled within seconds. While this speed delivers major benefits for consumers and businesses, it also introduces significant compliance challenges for financial institutions responsible for detecting sanctions risks.

Traditional sanctions screening processes were designed for payment systems where transactions could be paused for investigation. Instant payment infrastructures reduce or eliminate these delays. Banks must therefore detect potential sanctions matches and make investigation decisions almost immediately.

This creates a complex operational problem. Screening systems must analyse payment data in real time while maintaining the same level of regulatory compliance expected in slower transaction environments.

This guide explains why instant payment screening is challenging, how institutions adapt their screening systems to real time payment networks, and what operational practices help maintain reliable sanctions controls.

Why Instant Payments Change The Screening Environment

Instant payment systems settle transactions within seconds, leaving minimal time for traditional review processes. In many instant payment infrastructures, funds are irrevocable once the payment is processed.

Because of this, screening controls must operate before the payment is completed. Screening engines therefore need to analyse transaction data extremely quickly while maintaining high detection accuracy.

Regulators and international organisations recognise these challenges. Guidance discussed by the Bank for International Settlements on fast payments highlights how real time payment infrastructures require new approaches to risk management and compliance monitoring.

Financial institutions must therefore design screening systems that combine speed, accuracy, and operational resilience.

Where Instant Payment Screening Fits In The Transaction Pipeline

Screening controls operate directly within the instant payment processing workflow.

Payment Initiation

A customer initiates a payment through a digital banking channel.

Real Time Transaction Screening

Before the payment is approved, the transaction is evaluated by payment screening systems that compare the payment data against regulatory watchlists.

Alert Generation

If a potential sanctions match is detected, the system generates an alert.

Rapid Investigation

Compliance analysts review alerts through structured alert adjudication workflows that allow investigators to assess the match quickly.

Payment Approval Or Rejection

If the alert is cleared, the payment proceeds. If the match appears genuine, the payment may be blocked or escalated.

Because these steps occur within seconds, screening systems must be highly efficient.

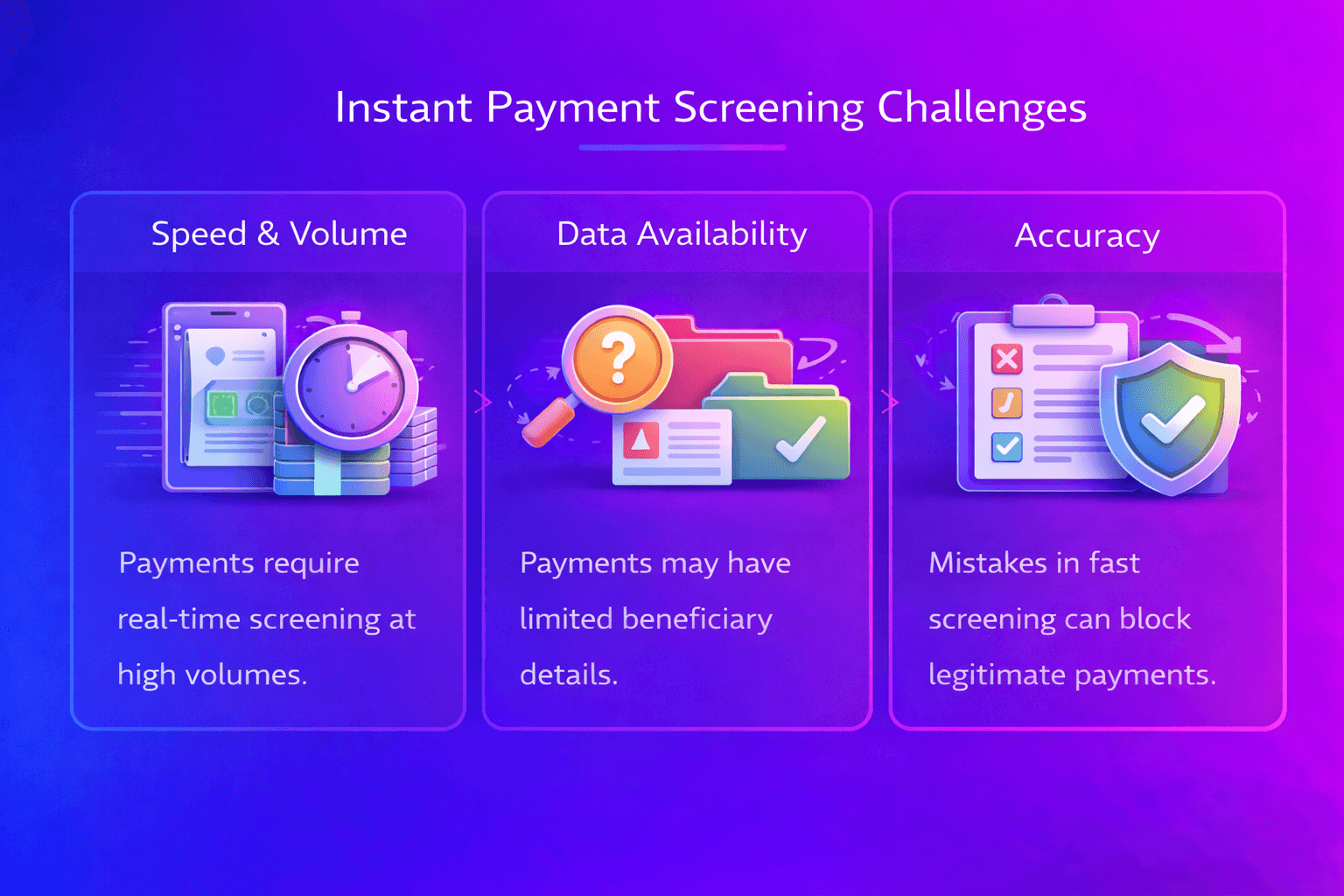

Core Challenges In Instant Payment Screening

Limited Investigation Time

Instant payment systems dramatically reduce the time available for investigators to review alerts. Compliance teams may have only a few seconds to decide whether a match is genuine.

High Transaction Volumes

Real time payment networks process extremely large volumes of transactions. Screening systems must therefore evaluate large numbers of payments without creating operational delays.

Data Quality Constraints

Instant payment messages may contain limited identifying information. When data fields are incomplete, screening systems must rely more heavily on name matching.

Managing False Positives

False positives become more problematic in instant environments because alerts must be resolved immediately. Excessive alerts can disrupt payment flows and frustrate customers.

Infrastructure Performance

Screening engines must operate with extremely low latency to avoid delaying payment processing.

These challenges require careful system configuration and operational design.

How Financial Institutions Adapt Screening Controls

Banks operating instant payment networks typically adopt several strategies to manage screening risk.

Optimised Matching Logic

Screening thresholds may be calibrated to prioritise higher confidence matches so alerts can be reviewed quickly.

High Quality Watchlist Data

Reliable sanctions data managed through a structured watchlist management platform allows screening systems to evaluate attributes more accurately.

Automated Risk Scoring

Some systems apply automated scoring to prioritise alerts based on risk indicators.

Investigator Decision Support

Investigation tools provide analysts with contextual information so decisions can be made quickly.

These practices help institutions balance compliance obligations with the operational demands of real time payment systems.

What Effective Instant Payment Screening Looks Like

Financial institutions that successfully manage instant payment screening typically demonstrate several characteristics.

Low Latency Screening Engines

Screening systems evaluate transactions within milliseconds to avoid delaying payment processing.

Reliable Watchlist Governance

Sanctions lists are maintained accurately so screening engines rely on high quality data.

Structured Investigation Workflows

Compliance analysts follow clear procedures when reviewing alerts.

Continuous Monitoring

Screening performance metrics are monitored to ensure detection accuracy remains strong.

These characteristics help maintain compliance controls within fast moving payment infrastructures.

Professional Insight And Operational Confidence

Instant payment screening highlights the tension between financial system speed and regulatory compliance. Payments must move quickly to support modern digital economies, yet institutions must still detect sanctions risks effectively.

Organisations that combine reliable data governance, efficient screening systems, and well trained investigators are better positioned to manage these challenges while maintaining confidence in their sanctions controls.

Practical Experience

Compliance practitioners often observe that improving data quality and investigation workflows significantly reduces operational pressure in instant payment environments.

Technical And Regulatory Expertise

Managing instant payment screening requires understanding both payment infrastructure and financial crime regulations.

Building Confidence In Controls

When screening systems operate reliably under real time conditions, institutions can demonstrate that their compliance frameworks remain effective even in high speed payment environments.

People First Compliance Content

Financial crime compliance ultimately depends on investigators who interpret alerts and make decisions about potential sanctions risks. While technology enables rapid screening of transactions, the strength of the compliance framework depends on how effectively analysts apply their expertise.

Educational resources like this aim to help compliance professionals understand how screening controls operate within modern payment infrastructures.

Next Steps For Your Organisation

Instant payment networks will continue to expand as financial institutions modernise their payment infrastructures. Ensuring that sanctions screening systems can operate effectively within these environments is therefore becoming increasingly important.

If your organisation is evaluating how its payment screening controls operate within instant payment systems, explore how your screening architecture compares with current industry practices.